In the Netherlands, average realized rents have risen by 13.9% since Q1 2020 and are expected to increase further in the next five years. Upward pressure on rents in a period of increasing supply might seem contradictory, but there are fundamental drivers supporting further growth.

Key headlines

· Average realized rents are increasing in The Netherlands

· Demand for high quality and ESG accredited space is driving further rental growth

· The limited development pipeline will ensure the Grade A market remains landlord favorable.

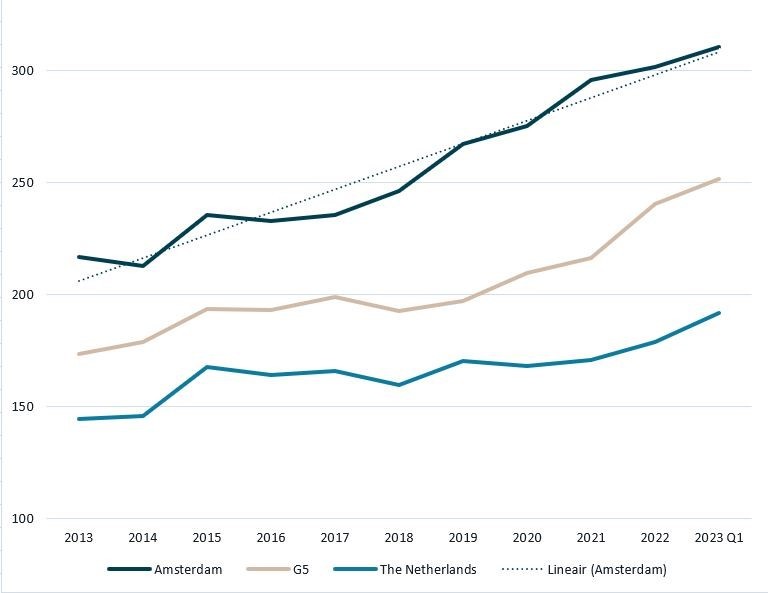

Dutch office rents have increased by 13.9% over the past three years

The Dutch office market continues to show strong fundamentals. In the five largest office markets of The Netherlands – Amsterdam, Rotterdam, Utrecht, The Hague, Eindhoven - (G5) the average realized rental value for lease transactions (larger than 500 m²) has risen by 19% since Q1 2020. Subsequently, in Q1 2023, the average rent in the G5 reached a record €252 /sqm/annum.

Inflation is pushing up costs, especially for new builds with developers and landlords who push this trough in new contract signings. Although inflation is partly fueling the upward trajectory of rental values in 2023 Q1, there are a host of other drivers at the root of the trend. See also the affordability of the commercial market - offices

Why are rents increasing?

Lease transactions suggest there is an increased focus on high-quality office space. This is partly due to corporates needing to emphasize the attraction of a joint space for their staff in order to pull people back from the home office. Furthermore, the ESG agenda is now more than ever a crucial variable in space requirements as more and more corporates set ambitious targets. Recent search requests support the view that there is still a need for (new) office space, but demand is concentrated around a small proportion of total stock due to the strict requirements. This is reflected in rents with the majority of the upward pressure confined to Grade A quality space, with best-in-class fit outs and state of the art systems.

This has resulted in a high demand for newly built, renovated and even existing A-grade offices in prime locations. In addition to the increased importance being placed on the build quality, location remains of great importance; excellent accessibility, amenitization and a mix of functions that ensure liveliness make the office attractive for occupiers. Office rents in locations that meet these requirements show an upward trendline. Examples of buildings that benefit from this include the Donna at Strijp-S in Eindhoven, WTC TowerTen at Zuidas Amsterdam, and The Cath and Central Park in Utrecht Centre.

Are rents increasing everywhere?

Whilst there is high demand for A-grade office space, the quality in supply is being hampered by a limited development pipeline. Although rental growth has been on the rise, it can be expected that in most other municipalities outside the G5, rental growth will be more subdued. Few buildings have been completed outside the core markets and the pipeline remains limited. In municipalities that are normally dependent on the relocation market (i.e. Tilburg), there is an inability to satisfy requirements within the municipality boundaries, which pushes for negative tenant migration.

Those occupiers who are eager to move have few options and are limited in the possibility to improve the quality of their office space when looking for new accommodation. This is a nonnegotiable given the costs of relocation and a new fit-out. In some municipalities, companies occupy outdated office space due to the absence of better alternatives. Since the immediately available supply is comparable to the occupier’s current office space, they are more likely to choose to extend their lease, which has a negative impact on the occupier dynamics and the development of rental value.

What’s to be expected for the next few years

In the upcoming 5 years, approximately 1.6 million sq m of leases in B/C grade offices will expire in The Netherlands; many of these occupiers will seek to upgrade their requirements to Grade A space. Demand for quality is fundamentally changing within corporations. Corporate commitments to net zero are bringing greater urgency to decarbonize real estate. The number of companies signing up to Science Based Target Initiatives (SBTi) has increased sixfold in two years and this will only intensify further. Those corporate targets even exceed the current quality available in key central business districts across The Netherlands. Zooming in on Amsterdam, expiring lease contracts of the large corporates and those signed up to SBTis) ambitions (note: approx. 200,000 sq m in 2023-2026) far exceed available supply. Just 40% can theoretically be accommodated by new, high quality ESG focused future supply planned to be delivered in 2023-2026.

The lack of substantial suitable stock will continue increase competition and drive further rental growth. For the near-term future, the office development pipeline in the Netherlands remains limited and will also continue to experience severe delays. With the collapse of the government in July 2023, it can be expected that a potential construction stop will intensify as decision-making on complex dossiers will be postponed to November 2023, when new elections will take place.

In addition to this, the difficulty in financing due to rising interest rates and lower yields, combined with insecurity around the nitrogen policy, can be expected to lead to planned developments experiencing further delays. This is likely to ensure a longer period of rental growth as demand will continue to outstrip supply. The supply-demand imbalance suggests a further polarization of the Dutch offices landscape. The top 20% of the market will continue to prosper while Grade B, C and badly located space encourage dwindling demand, higher vacancy, and erosion of rents. The tight supply at the top-end does present opportunities as well. Well-located Grade B offices will most likely be targeted for refurbishment to alleviate some of the demand pressure.